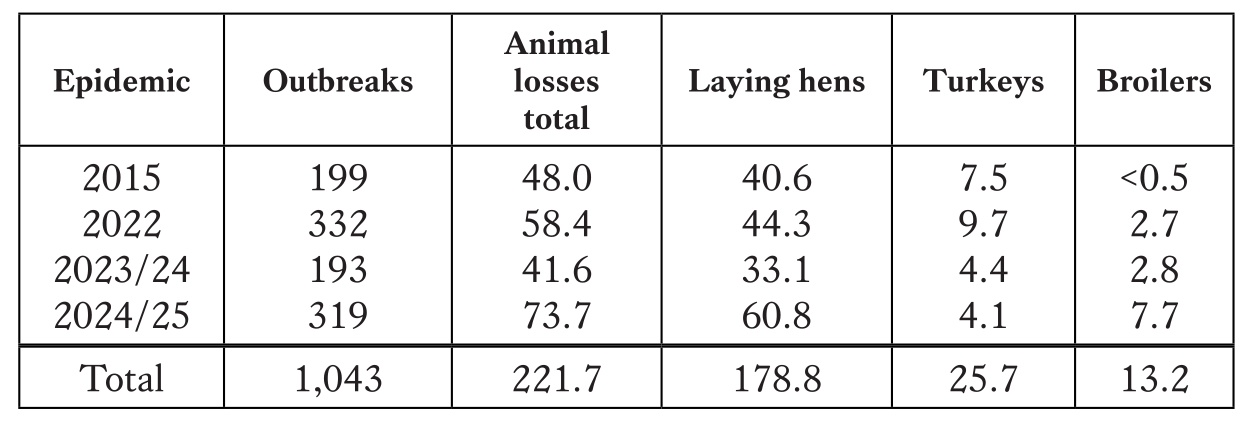

Between December 2014 and July 2025, the U.S. poultry industry has been hit by four devastating outbreaks of avian influenza (AI). In total, the highly pathogenic AI virus (HPAI) was diagnosed on 1,043 commercial poultry farms (1,932 total farms, including backyard flocks). A total of 221.7 million poultry died due to viral infection or preventive culling. Of these birds, 178.8 million were laying hens, 25.7 million turkeys and 13.2 million broilers (Table 1). In a first paper (Zootecnica Poultry magazine, December 2025) the impacts of the epidemics on the egg industry were analysed. In this article, the temporal and spatial spread of the disease, its economic impact on poultry meat production and the responses of the industry and the government are documented.

Major differences in the number of outbreaks and animal losses

Source: APHIS.

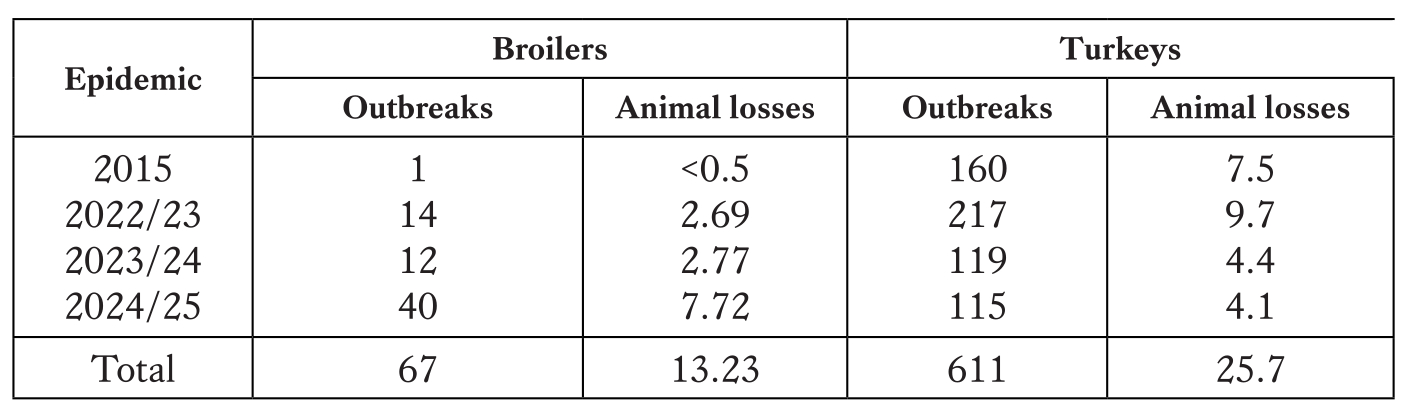

A comparison of outbreaks and animal losses in turkey and broiler production reveals major differences. 611 outbreaks occurred on turkey farms, compared to 67 on broiler farms. In total, 25.7 million turkeys fell either victim to the disease or to preventive culling and 13.2 million broilers were lost. The differences between the four epidemics are remarkable (Table 2). While the number of infected broiler farms was still quite low in the first three epidemics, it more than tripled in the last one. Outbreaks in turkey flocks were very high in all four epidemics, but declined during the last two. This trend is also reflected in animal losses. Among broilers, losses increased sharply between 2023/24 and the following epidemic, while among turkeys they decreased.

Source: own calculations based on APHIS data.

The reasons for the differences cannot be discussed in detail here, but are discussed in another paper1. In addition to the types of housing, important reasons included the size of the flocks, the different lengths of the fattening periods, the regional patterns of turkey and broiler growing, the flyways of wild birds and the susceptibility of poultry species to the AI virus. While turkeys for meat production were still housed in open barns in the middle of the last decade, especially in the northern Midwest, closed facilities were only gradually becoming established. In contrast, broilers in large flocks had always been kept in closed barns. In the south-eastern United States, the centre of broiler growing, they were frequently kept however on small farms in so-called Louisiana houses, whose side walls could be closed with curtains. The flyways preferred by wild birds played an important role.

The flyways along the Pacific coast (Pacific Flyway) and in the Mississippi Valley (Central Flyway) were highly frequented, in contrast to the flyway along the Atlantic coast. The south-eastern United States and the states in the Lower Mississippi Valley were only rarely reached by wild birds. Where the centres of production coincided with the flyways, large numbers of infections and high animal losses occurred, as was the case in 2015 and in 2022/23 in the Midwest and in 2024/25 in the Pacific states.

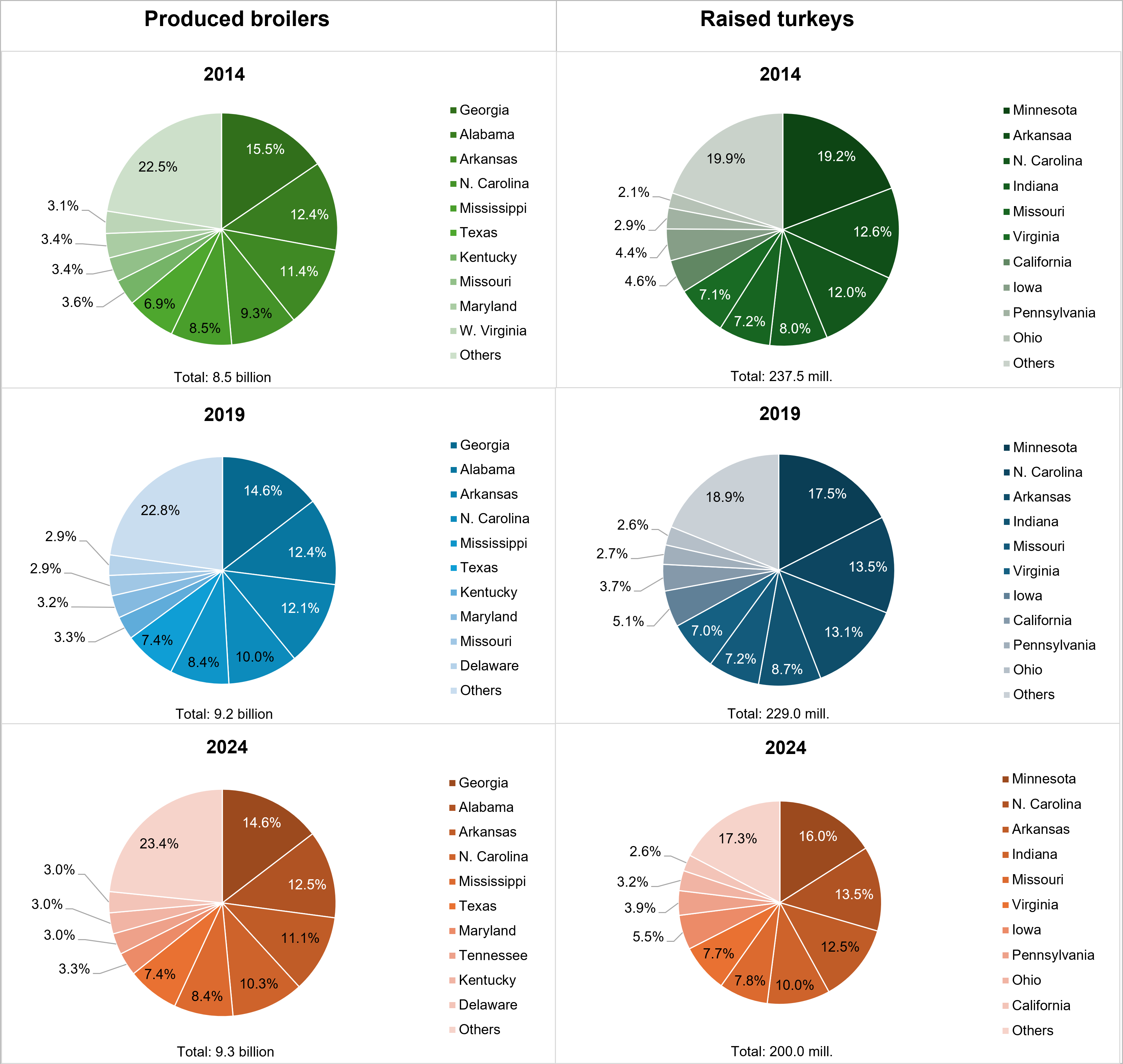

Changes in the regional pattern of production

Considering the high animal losses, one might have expected that this would have led to a fundamental change in the spatial structure of poultry farming in order to reduce the risk of infection. However, as Figure 1 shows, this has only happened to a limited extent so far. Broiler farming continues to be dominated by the states on the Mid-Atlantic Coast, in the Southeast and in the Lower Mississippi Valley. In addition, a secondary centre has formed in California. In turkey farming, the Midwest and some states on the Mid-Atlantic coast occupy the leading positions. Here, too, a sub-centre has developed in California. Why these centres have formed cannot be explained in detail here, but can be found in two papers of the author (Windhorst 2002, 2025b).

Design: A. S. Kauer based on data of USDA, NASS Poultry Production and Value.

The regional focus of poultry farming reflects the location of the leading companies in slaughtering and processing. Vertical integration, which usually combines all phases from hatchery via contract fattening to slaughtering and processing under one company umbrella, has resulted in regional concentration. Capital investment, labor availability, and grower expertise cannot be easily relocated. Although Minnesota has suffered high losses in turkey farming and Georgia in broiler farming, little has changed in the basic spatial structure, with the exception of California. There, massive animal losses in the winter of 2024/25 brought broiler farming production to a virtual standstill and almost halved the share of turkey farming in U.S. production.

Different impactson production

In a further step of the analysis, the impacts of the four epidemics on turkey and broiler production will be analysed.

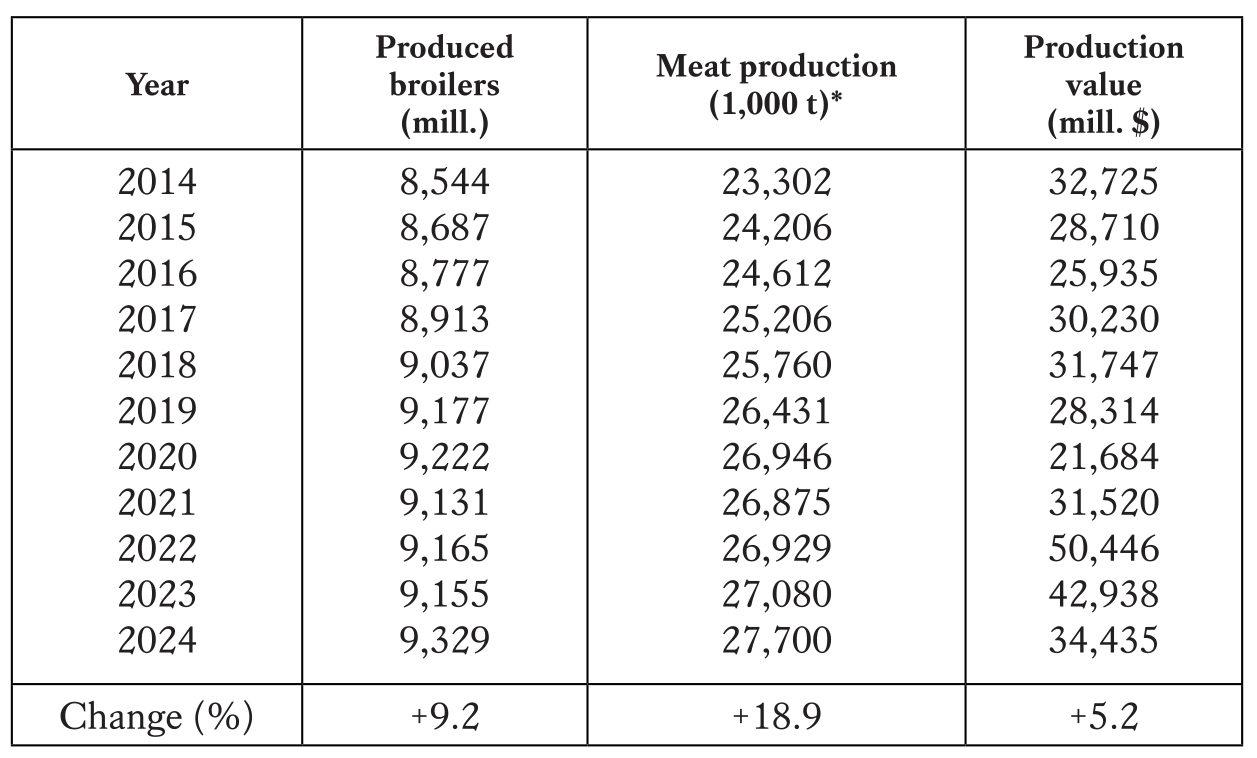

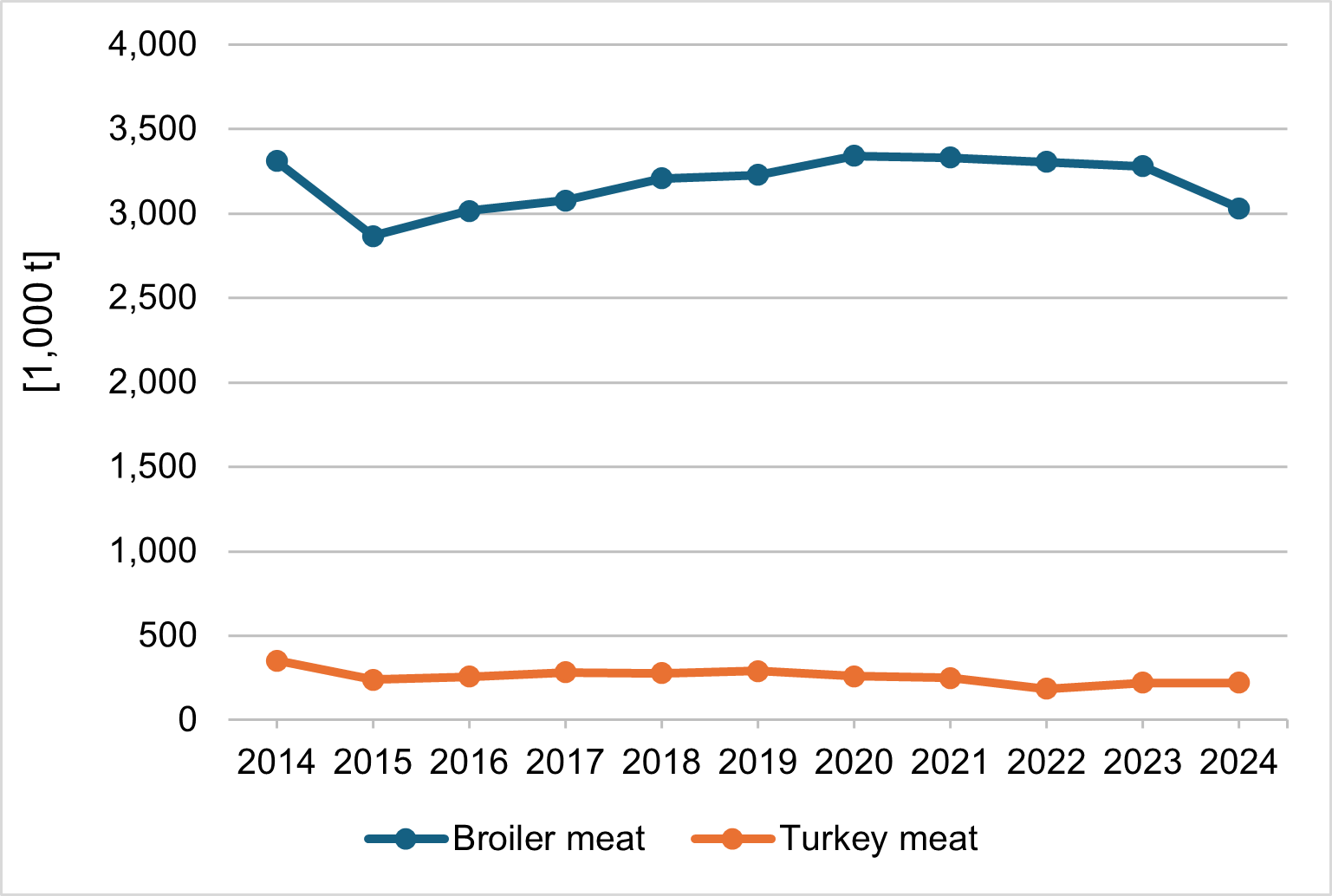

Table 3 shows that the number of broilers produced has increased steadily over the decade under review, apart from a slight dip in 2021 as a result of the COVID-19 pandemic. The production volume increased from 8.5 billion to 9.3 billion birds, or by 9.2%. Similarly, broiler meat production also grew. Here, a slight decline occurred in 2021. The impact of the epidemic in the winter half-year 2024/25 on meat production can only be estimated as no precise data is available yet. The loss of 7.7 million broilers and the fact that some barns stood empty for months, because they were not approved for restocking, are likely to reduce the number of animals produced to less than 9.3 billion by the end of 2025 and meat production by around 80,000 tonnes. The value of produced broiler meat fluctuated considerably during the decade analysed here. At $21.3 billion, the lowest value was achieved in 2020 towards the end of the COVID-19 pandemic, while the highest value of $50.4 billion was achieved in 2022 during the second AI epidemic. Changes in domestic demand and on the global market were the most important steering factors.

Source: USDA NASS. Poultry Production and Value.

*Live weight

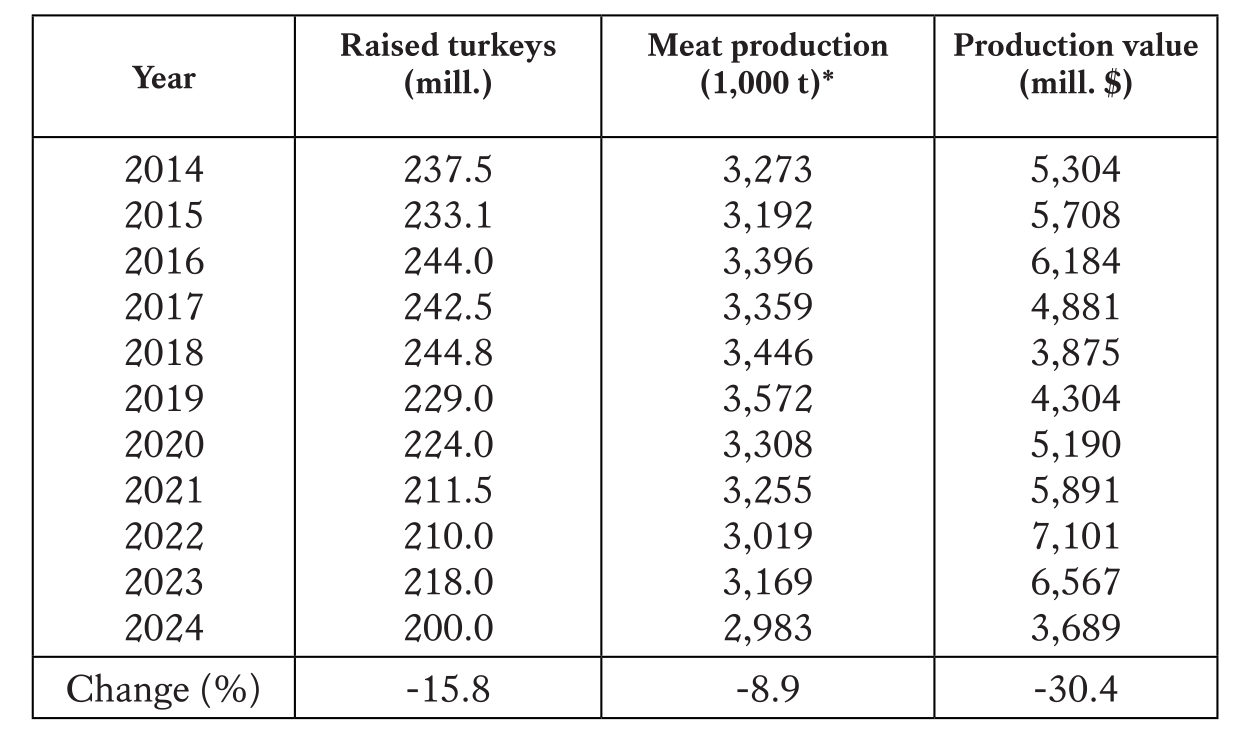

In 2014, before the first major AI epidemic, 237.5 million turkeys or 3.27 million tonnes of turkey meat worth $5.3 billion were produced (Table 4). The outbreaks caused production to decrease by around 4 million animals or 81,000 tonnes. In the following years, production rose again to 244 million, but then collapsed again during the COVID-19 pandemic and fell to only 200 million due to the two subsequent epidemics. Between 2018 and 2024, turkey production decreased by 18.1% and meat production by 12.9%. Due to the shortage in supply, the production value rose to $7.1 billion in 2022, but then fell to just $3.7 billion by 2024, a decline of 48.0%. Another reason for the continuing downward trend was certainly the decrease in per capita consumption from 7.2 kg in 2016 to only 6.3 kg in 2024. For 2025, the USDA predicts a decline in production to 2.27 million tonnes.

Source: USDA NASS. Poultry Production and Value.

*Live weight

Considerable decline in poultry meat exports

The four AI epidemics had massive impacts on exports of broiler and turkey meat, as leading importing countries immediately stopped their imports. While the poultry industry was able to recover relatively quickly after the 2015 epidemic, this was not the case with the three epidemics that followed in quick succession from 2022 onwards, because a number of countries did not reopen their borders to imports over the whole time period.

A comparison of export trends for broiler and turkey meat (Figure 2) reveals some notable differences. Exports of broiler meat fell by more than 440,000 tonnes, or 13.4%, between 2014 and 2015, only returning to their initial level in 2019. The value of exports decreased by $1.2 billion between 2014 and 2016. Between 2023 and 2024, exports fell again by 250,000 tonnes, but higher average prices were achieved in the remaining markets. While only about $950 per tonne was earned in 2016, the average value per tonne rose to $1,400 in 2024. However, only those farms that were not affected by an infection were able to benefit from this increase. The extent to which exports slumped after the outbreak wave in the winter half-year 2024/25 will only become obvious in a few months’ time when detailed statistics are available.

A comparison of export trends for broiler and turkey meat (Figure 2) reveals some notable differences. Exports of broiler meat fell by more than 440,000 tonnes, or 13.4%, between 2014 and 2015, only returning to their initial level in 2019. The value of exports decreased by $1.2 billion between 2014 and 2016. Between 2023 and 2024, exports fell again by 250,000 tonnes, but higher average prices were achieved in the remaining markets. While only about $950 per tonne was earned in 2016, the average value per tonne rose to $1,400 in 2024. However, only those farms that were not affected by an infection were able to benefit from this increase. The extent to which exports slumped after the outbreak wave in the winter half-year 2024/25 will only become obvious in a few months’ time when detailed statistics are available.

Turkey meat exports fell by 111,500 tonnes or by 31.7% between 2014 and 2015, with the export value decreasing by $177.3 million. Although the export value fluctuated considerably in the subsequent years, partly due to the COVID-19 pandemic, it did not reach the initial level again. There was a further significant decline in exports of 64,000 tonnes as a result of the AI outbreaks in 2022. As with broiler meat, the export value only decreased by $25 million. Here, too, a much higher price of $3,470 per tonne was achieved on the world market than in 2015, when the price was as low as $2,455. However, this value could not be maintained in the following two years.

Considering the expected increase in global demand for broiler meat, export volumes are likely to rise in the coming years, unless another wave of AI outbreaks restricts export opportunities. However, the USA faces increasing competition from Brazil and some EU member countries. Turkey meat exports will continue to decline in view of the high animal losses caused by the epidemic in the winter of 2024/25. The situation is exacerbated by the fact that import restrictions in important buyer countries remain in place because further AI outbreaks occurred in Arizona and Pennsylvania in June and July 2025.

The legislature responds

Although it was primarily the shortage of eggs in food retail stores and the sharp rise in egg prices that led to protests among the population and forced the government to take action, the high animal losses caused by the AI virus and the extensive preventive culling also led to a critical attitude. There was also a lack of understanding that individual farms and companies, which were repeatedly affected by infection, were nevertheless compensated for their losses with tax money.

In December 2024, APHIS responded with a new guideline that makes future compensation payments for animal losses due to AI infection subject to certain conditions2. For example, it requires that a farm can only be restocked if an improvement in biosecurity has been demonstrated. This has to be verified by an APHIS audit. The new legal regulation is intended to improve the biosecurity on poultry farms3.

On 18 February 2025, a group of 16 senators from both parties sent a letter to the Secretary of Agriculture calling for the development of a forward-looking strategy in the development of vaccines and their use in laying hen and turkey farming4.

In response, the US Department of Agriculture provided $100 million in April 2025 to enable scientists to develop new vaccines to protect poultry stocks and to research the transmission routes of the AI virus in wild birds and its spread in poultry and livestock. The aim is to limit the extent of recurring epidemics, if not prevent them altogether. In addition, $500 million was allocated to improve biosecurity on farms and $400 million to support farms that were particularly affected5.

In March 2025, a working group, consisting of representatives from industry, trade organisations and state veterinarians, met to develop a plan for the vaccination of poultry. It is to be published in July 2025 and sent to the Secretary of Agriculture and industry organisations in the poultry sector for comment6. So far, nor results have been available. Whether broiler farmers will give up their resistance to vaccination, which they have justified since 2014 with fears of import bans by leading buyer countries, remains an open question.

Summary and outlook

Four epidemics of the highly pathogenic avian influenza have affected poultry farmers in the United States over the past decade. A total of 1,043 outbreaks in commercial farms resulted in the loss of almost 222 million animals, either due to infection or by preventive culling. The high economic losses suffered by farms and the processing industry, as well as supply problems for the population, forced the government to take action. In addition to providing research funds for the development of vaccines, a plan for preventive vaccination is to be developed and adopted in consultation with the poultry industry. However, the leading poultry meat companies are unlikely to give their approval unless it can be guaranteed that vaccination will not result in import bans by the most important receiver countries. The ongoing threat to poultry stocks will force the poultry industry to improve the biosecurity of their barns. This will require a reorientation on the part of the small farmers as well as the managers of large farm complexes, as they have for a long time felt a false sense of security and underestimated the threat posed by the AI virus.

Data sources and supplementary literature

Congressional Research Service. The Highly Pathogenic Avian Influenza (HPAI) Outbreak in Poultry, 2022–Present. Washington, D.C., 2025. Available at: https://www.congress.gov/crs_external_products/R/PDF/R48518/R48518.1.pdf

National Chicken Council. Industry Facts and Stats. Available at: https://www.nationalchickencouncil.org/industry/statistics

National Turkey Federation. Annual Reports. Available at: https://www.eatturkey.org/category/annual-report

USDA, FAS. U.S. Foreign Agricultural Trade. Available at: https://apps.fas.usda.gov/gats/default.aspx?publish=1

USDA, NASS. Poultry Production and Value. Annual Summaries. Available at: https://www.nass.usda.gov/Publications/Todays_Reports/reports/plva0425.pdf

U.S. Poultry & Egg Association. Economic Data. Available at: https://www.uspoultry.org/economic-data

Windhorst, H.-W. (2002). The Old South goes poultry and pigs – Neuausrichtung der Agrarproduktion im Alten Süden. In W. Klohn & H.-W. Windhorst (Eds.), Die Land- und Forstwirtschaft im Alten Süden der USA (Vol. 23, pp. 113–150). Vechta.

Windhorst, H.-W. (2023). Two waves, different routes and changing dynamics: The avian influenza outbreaks in the USA in 2022. Poultry World, 39(2), 8–11.

Windhorst, H.-W. (2024). Third avian influenza outbreak in the USA within 10 years: The 2023–2024 epidemic. Zootecnica International, 46(9), 28–33.

Windhorst, H.-W. (2025a). Fourth AI epidemic in the USA in the past decade: The epidemic in winter 2024/25. Zootecnica International, 46(7–8), 20–26.

Windhorst, H.-W. (2025b). Fleischerzeugung und -handel der USA. Teil 1: Dynamik und Struktur der Fleischerzeugung der USA zwischen 2019 und 2024. Fleischwirtschaft, 105(6), 30–34.

Windhorst, H.-W. (2025c). Fleischerzeugung und -handel der USA. Teil 2: Dynamik und Struktur des Fleischhandels zwischen 2019 und 2024. Fleischwirtschaft, 105(6), 22–25.

Windhorst, H.-W. (2025). The U.S. poultry industry under stress. Part 1 – The egg industry. Zootecnica Poultry magazine, December.

Notes

Windhorst 2023, 2024 2025.

https://www.aphis.usda.gov/print/pdf/node/7419

https://www.aphis.usda.gov/news/agency-announcements/aphis-announces-updates-indemnity-program-highly-pathogenic-avian

https://www.ernst.senate.gov/imo/media/doc/letter_to_usda_in_response_to_hpai_outbreaks.pdf

Irritating in this context are statements by the Secretary of Agriculture, Rollins, and the Secretary of Health and Human Services, Kennedy, who no longer favoured the development of vaccines and preventive vaccination to combat AI. Secretary Kennedy suggested that herds should not be culled preventative but be infected so that breeding lines could then be established with the surviving animals because they had apparently developed resistance. There was massive opposition to this from the poultry industry. See The Highly Pathogenic Avian Influenza (HPAI) Outbreak in Poultry, 2022-Present, p. 10, https://www.congress.gov/crs_external_products/R/PDF/R48518/R48518.1.pdf

Personal information from Dr. Denise Heard, Vice President Research, U. S. Poultry & Egg Association (July 7th, 2025).