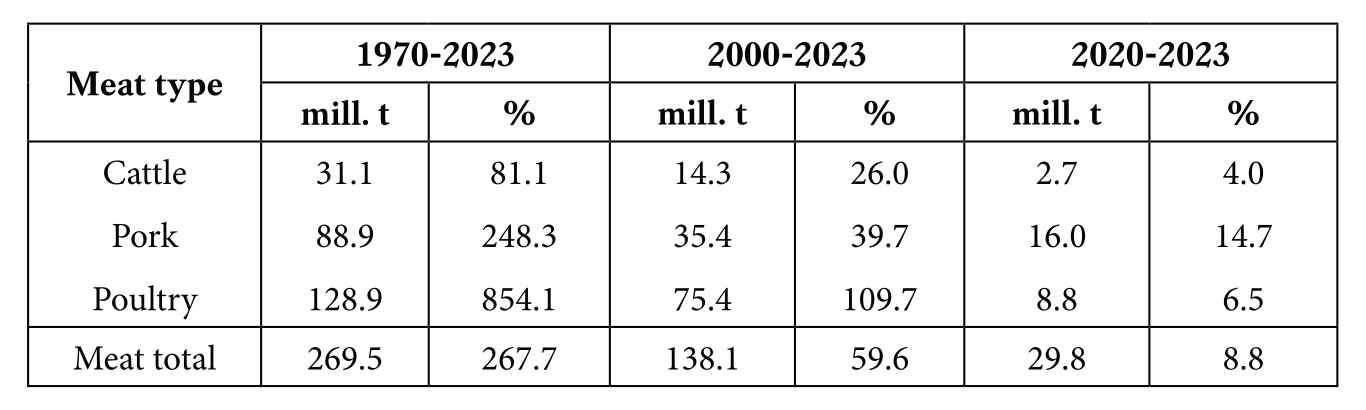

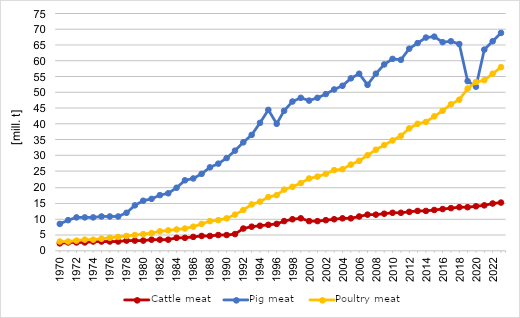

Global meat production increased by almost 270 million mt1, or 268% between 1970 and 2023. Examining the development by meat type reveals that the dynamics was primarily driven by the rapid increase in poultry meat production. However, it is worth noting that this meat type has not dominated between 2020 and 2023. This article analyses the longer-term trends and the dynamics since 2000 in detail.

Long-term trends. The success story of poultry meat

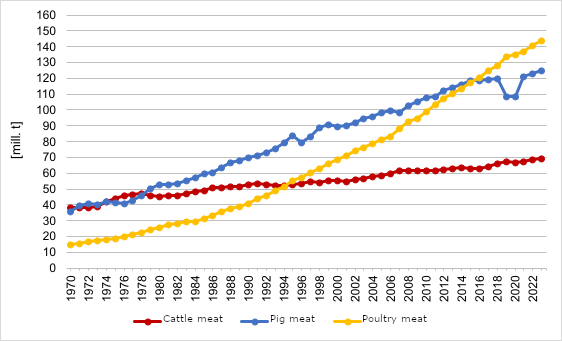

Analysing the long-term development for the three most important meat types and time periods reveals some striking changes. Obviously, poultry meat production has grown significantly faster than red meat production. The author has characterised this dynamic as a ’red-white shift’ (Windhorst, 2021). Table 1 shows that between 1970 and 2023 the absolute growth in poultry meat production was nearly as high as that of the two most important types of red meat combined. The same applies to the period from 2000 to 2023. However, the picture changes when only the short-term development between 2020 and 2023 is considered. Here, pig meat production grew significantly faster than that of poultry meat. This can be explained by the rapid increase of production in China and Brazil. Following the containment of African swine fever, Chinese production rose by 16.8 million mt over four years, and Brazilian production increased by almost 1 million mt due to a greater focus on exports. A more detailed analysis will follow in a later section.

Source: FAO data.

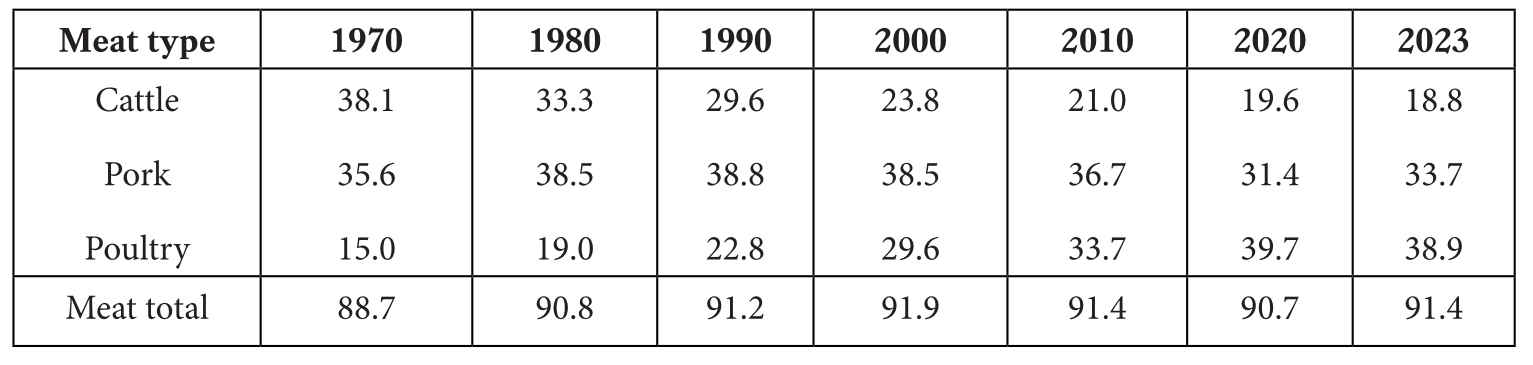

When examining the long-term change of the share of beef, pork and poultry in global meat production, a shift towards white meat becomes apparent (Table 2, Figure 1). Between 1970 and 2023, beef lost 19.3% of its original share. In contrast, pig meat has remained relatively stable. Poultry gained 23.9%, making it the big winner, although it lost 0.8% between 2000 and 2023.

Source: FAO data.

Design: A. S. Kauer based on FAO data.

Medium-term development. The growing dominance of Asia

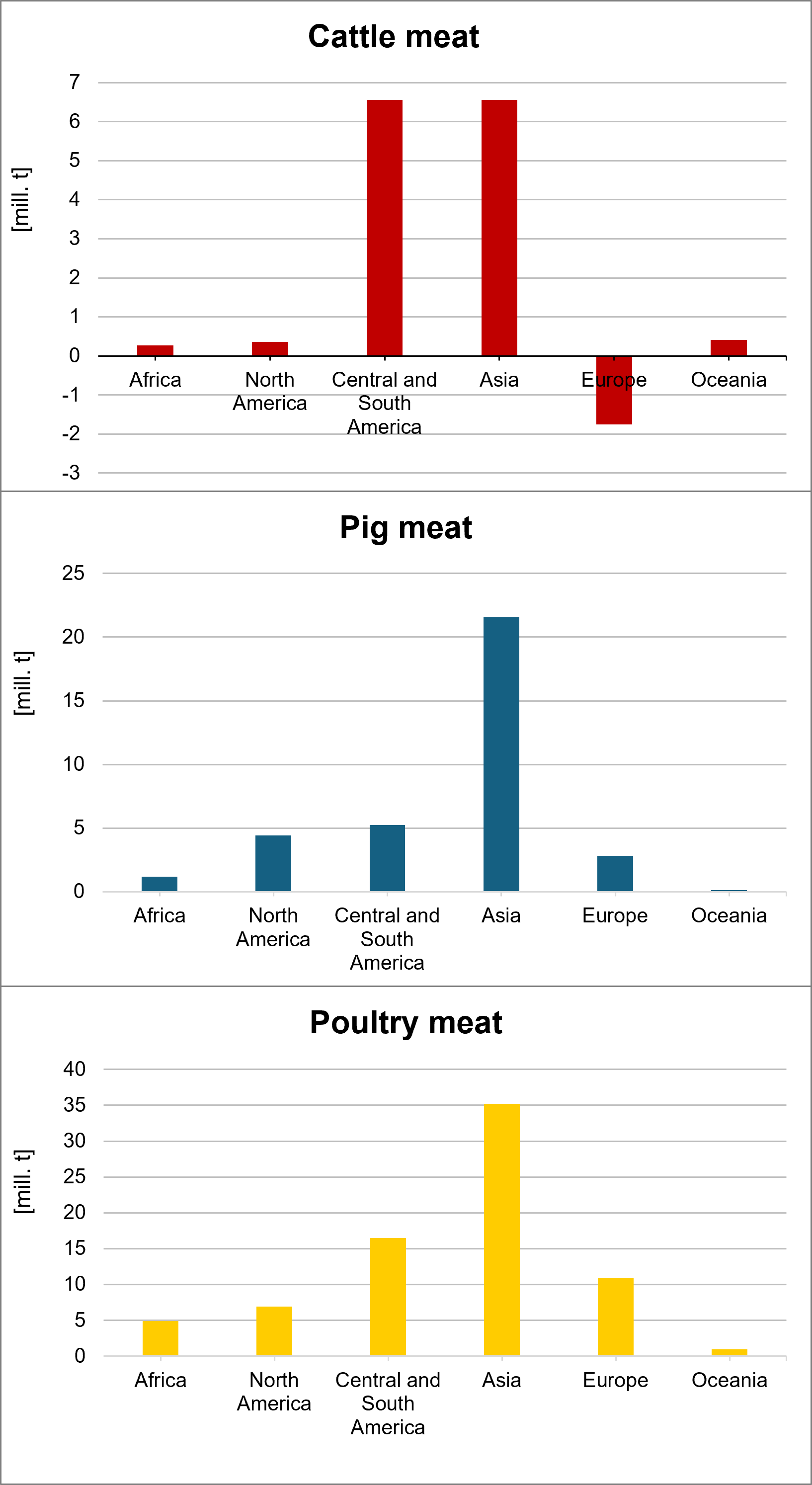

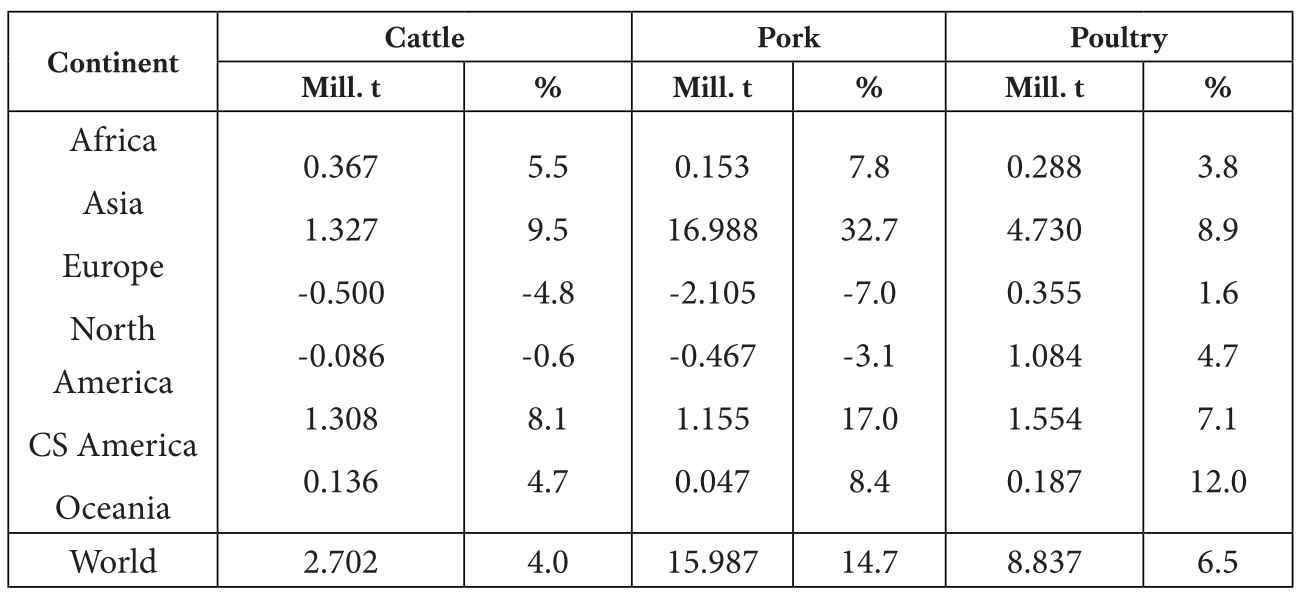

This part of the analysis analyses how meat production developed by meat type and continent between 2000 and 2023. Figure 2 shows that the contribution by the individual continents to this development varied considerably. For beef, the absolute increase in Asia and Central and South America was almost the same. The contribution of the other continents was comparatively insignificant, with Europe even recording a decline of 1.8 million mt. Asia was an exception with pork production increasing by 21.5 million mt. It was followed by North and South America and Europe. Although Africa continued to account for only a small proportion of global production, its share doubled between 2000 and 2023. Pig meat remained of minor importance in Oceania. At 35.2 million mt, Asia showed the largest growth in poultry meat production, followed by Central and South America at 16.9 million mt, and Europe at 10.9 million mt. At first glance, the significantly lower increase in North America seems surprising. However, it has to be noted that the two North American countries accounted for already 17.9% of the global production volume in 2000. Africa showed a remarkable dynamic, increasing its production by around 5 million mt. Oceania lagged far behind the other continents in terms of this meat type, reflecting its small population.

Design: A. S. Kauer based on FAO data.

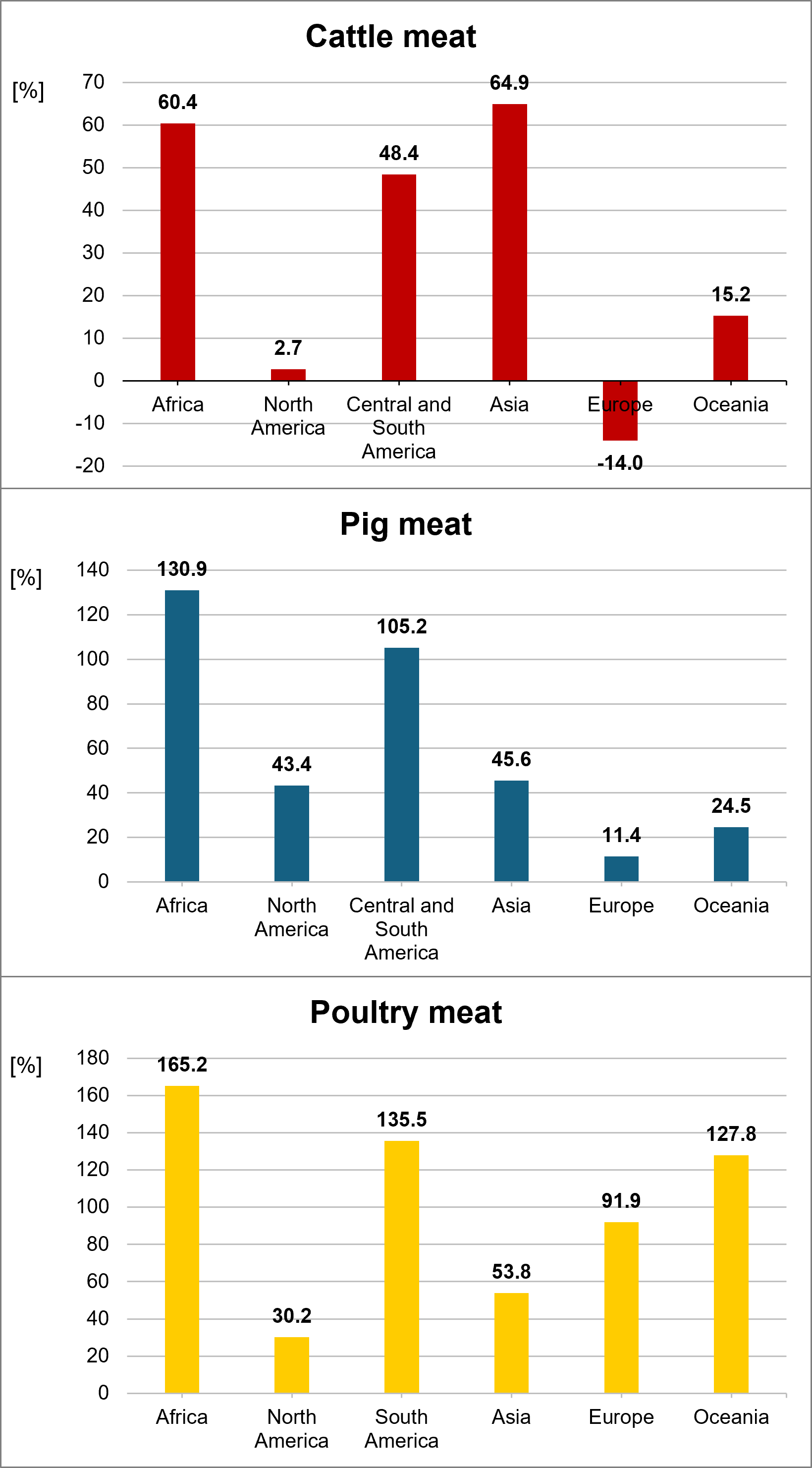

A different picture emerges when the relative change in meat production is analysed (Figure 3). Asia and Africa achieved relative growth rates of over 60% for beef, followed by Central and South America with 47.8%. North America recorded the lowest growth rate of only 2.7%, apart from Europe’s downward trend. North America’s low growth rate reflects the declining per capita beef consumption in the USA. While it had been as high as 30 kg in 2000, it had fallen to 27 kg by 2023. The high retail price compared to pig meat and, in particular, broiler meat was the decisive steering factor.

Design: A. S. Kauer based on FAO data.

Africa showed the highest relative increase in pork production at 130.9%, followed by Central and South America at 105.2%. Growth was much lower in Asia and North America, here, the already high baseline figures for 2000 must be taken into account. Europe ranked last with an increase of only 11.4%, reflecting the slight increase in per capita consumption. In some countries, consumption has been stagnating or even declining for years, because consumers preferred poultry meat for its lower retail price, while that of beef had risen sharply.

Poultry meat achieved the highest relative growth rate in Africa at 165.2%, followed by Asia at 153.8%, and Central and South America at 142.1%. Oceania’s high figure must be viewed in the context of its low baseline of just 0.77 million mt produced in 2000.

In summary, Africa and Central and South America showed a remarkable dynamic. Asia was only in the top position for beef production. The comparatively low momentum in North America is surprising at first glance. Here, meat consumption has obviously reached a saturation point in the USA, and growth can only be achieved through population growth or higher exports. Africa’s dynamic development is due to the rising per capita income of a growing middle class in some North African countries and South Africa. Central and South America demonstrated a remarkable growth across all three meat types, with Brazil’s increased exports playing a pivotal role.

What about short-term trends, a resurgence of pork?

Looking at the short-term trend in global meat production between 2020 and 2023 reveals some remarkable developments. The fact that consumption options were restricted in many countries during the Covid-19 pandemic resulted in changing preferences of the consumers for meat types.

Between 2020 and 2023, global production of the three main meat types increased by 27.5 million mt. Approximately 16 million mt or 58.1% of this was pork, 8.8 million mt respectively 32.1% was poultry, and 2.7 million mt or 9.8% was beef. Does this development spell the end of poultry meat’s success story? Examining the data for individual continents (Table 3) reveals that the increase in pork production was primarily driven by developments in Asia and, to a much lesser extent, in Central and South America. In contrast, the production volume in Europe and North America fell by around 2.6 million mt in total, with Europe accounting for 2.1 million mt of this decline. The containment of African swine fever boosted pork production in Asia, offsetting the 16 million mt slump between 2015 and 2020. A comparison of the production volumes in 2015 and 2023 reveals that production increased by only 1.5%. In contrast, beef production grew by 18.3%, and poultry meat even by 36.9%. While beef production in Asia and Central and South America increased by a combined 2.7 million mt, it declined by 0.6 million mt in Europe and North America. Of all meat types, on ly poultry showed positive growth across all continents. Figure 4 clearly documents that in Asia the dynamic of this meat type remained unaffected. The sharp increase in pork production since 2020 was merely a short-term response to the significant losses caused by the African swine fever outbreaks in China and several other Asian countries between 2018 and 2020.

ly poultry showed positive growth across all continents. Figure 4 clearly documents that in Asia the dynamic of this meat type remained unaffected. The sharp increase in pork production since 2020 was merely a short-term response to the significant losses caused by the African swine fever outbreaks in China and several other Asian countries between 2018 and 2020.

Source: FAO data.

Design: A. S. Kauer based on FAO data.

Conclusion. Asia and Central and South America dominated

Besides comparing the absolute and relative growth of global meat production, it is of interest to examine how much each continent contributed to the total production as well as to the production of the three most important meat types. Figure 5 provides a summary of this.

Between 2000 and 2023, Asia contributed 55.6% to the 138.1 million mt growth in global meat production, with Central and South America contributing a further 17.9%. These two continents thus accounted for almost three-quarters of the increase. In contrast, the significantly lower growth in Europe and North America is reflected in their combined share of only 17.1%.

A similar pattern emerges when looking at individual meat types. Once again, Asia and Central and South America were in the leading positions. During this period, the two continents contributed 69.2% to the increase in poultry meat production, 75.6% to pork production, and 92.5% to the increase in beef production. It is worth noting that Oceania had an even higher share in beef production than Europe or North America.

The dynamics of global meat production reflect both population size and the continents’ respective shares in the world population. In 2023, Asia accounted for 59% of the world’s population, while Central and South America accounted for 8% and Europe and North America for 14%. Africa achieved the highest relative population growth between 2000 and 2023, at 83%, while Europe had the lowest, at only 2.8%. Given the emerging population dynamics and economic development, it is reasonable to assume that Asia and Central and South America will increase their shares in global meat production, while Europe and North America will lose shares.

Data sources and supplementary literature

FAO. FAOSTAT. https://www.fao.org/faostat

World Population Review. Continents. https://worldpopulationreview.com/continents

Windhorst, H.-W. (2021). The red-white shift in global meat production. Zootecnica International, 43(5), 32–37.

Windhorst, H.-W. (2024). Was it the decade of Asia? The dynamics of global meat and egg production between 2012 and 2022. Meatingpoint, (54), 60–64.

Windhorst, H.-W. (2024). South America – the continent of cattle and chickens. Meatingpoint, (55), 12–15.

Windhorst, H.-W. (2025). Oceania – disadvantage of peripheral location. Fleischwirtschaft International, (1), 14–21.

Windhorst, H.-W. (2025). ASEAN – The dynamics of the meat industry. Fleischwirtschaft International, (2), 46–51.

Note

1 mt: metric tonne (= 1,000 kg)