The USDA semi-annual report on EU poultry forecasts growth in chicken meat production for 2026. It highlights production gains amid easing disease pressures and steady demand.

Production growth

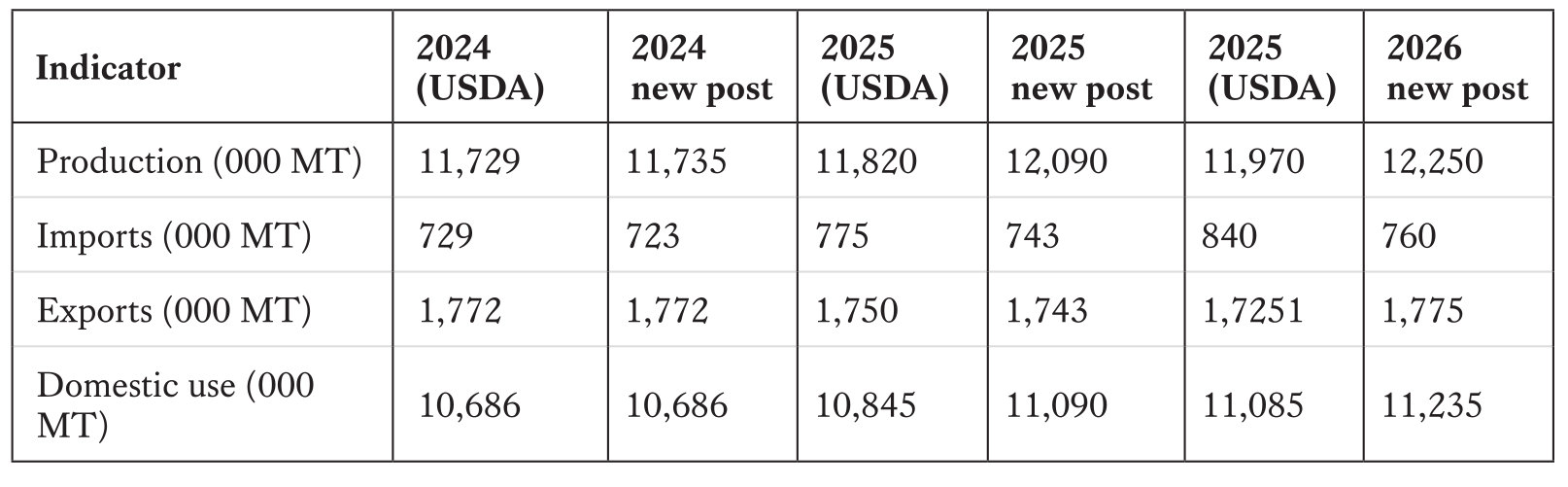

EU chicken meat production is projected at 12.25 million metric tons (MT) in 2026, up from 12.09 MT in 2025 and 11.73 MT in 2024 (Table 1). This uptick stems from robust domestic demand, fewer high-pathogenicity avian influenza (HPAI) outbreaks, and lower energy and feed prices supporting producers’ income, especially in top producers Poland, that holds over 22% of total EU output despite health challenges.

Environmental caps limit gains in the Netherlands, Belgium, and Germany via nitrogen emission rules.

Rising consumption

Domestic consumption climbs 1.4% to 11.235 MT in 2026, fueled by retail and HRI (hotels, restaurants, institutions) sectors. Chicken’s appeal as an affordable, healthy, versatile protein persists over red meats, aligning with long-term trends in price sensitivity and wellness. HRI demand particularly lifts per-capita intake across the EU.

Trade dynamics

Imports edge up 1% to 760,000 MT in 2026 after a 5.4% growth in 2025, driven by HRI needs. The UK remains top supplier but faces post-Brexit checks and imports declined by 8% in 2025; Ukraine stabilizes at 136,000 MT under revised DCFTA (Deep and Comprehensive Free Trade Agreement) quotas from October 2025, curbing sensitive products. Thailand (+16%) and China (+36%, over 55,000 MT for Asian HRI) gain share thanks to lower competition from Ukraine, while Brazil hits EU quota limits.

Lower-priced Ukrainian chicken meat and ongoing HPAI and ND outbreaks may continue to restrain EU exports, while lower production costs support competitiveness.

In 2026 exports are expected to rise by 2% to 1.775 MT, rebounding from 2025’s 2% dip due to HPAI/ND curbs. Losses in Vietnam (-14%) and Saudi Arabia (-21%) are offset by gains in Ghana (+15%), DR Congo (+23%), and Philippines (+65%). The UK leads markets; low costs could boost dark meat competitiveness in sub-Saharan Africa.

The EU has recently finalized and rolled out several free trade agreements (FTAs) that include concessions on livestock products. First of all, Mercosur, for whom negotiations wrapped up in December 2024, leading to formal signatures in January 2026 in Asunción, Paraguay, by representatives from the EU and the Mercosur countries (Argentina, Brazil, Paraguay, and Uruguay). The deal splits into an Interim Trade Agreement covering trade and investment, plus a broader Partnership Agreement. It features strong bilateral safeguard clauses to shield EU agriculture from market disruptions, with the European Parliament approving rules in February 2026 that allow tariff suspensions if sensitive product imports rise more than 5% above a three-year average. Duties will phase out gradually on 91% of EU exports to Mercosur and 92% of their exports to the EU, though the agreement is now under legal review by the European Court of Justice at Parliament’s request to check treaty compatibility.

For Ukraine, the EU offered temporary trade liberalization through Autonomous Trade Measures (ATMs) from June 2022 until June 2025. After that, relations reverted to the original 2014 DCFTA under Regulation 1132/2025, reimposing quotas on Ukrainian agricultural goods until late October. The revised DCFTA then took effect on October 29, 2025 (Regulation 2025/2199), expanding mutual market access beyond 2014 levels while capping EU imports of sensitive products compared to the ATM period. It adds a new safeguard mechanism and aligns Ukrainian production standards with EU rules.

Key EU policies

CAP simplification (May 2025) simplify administrative burdens and environmental requirements linked to eco-payments, effective 2026. Omnibus food safety law (December 2025) includes provisions requiring imported products to meet EU environmental, food safety, and animal welfare standards, in line with the “mirror clause” approach.

On the trade front, significant shifts are underway: the revised Ukraine DCFTA introduces caps on sensitive imports, while the Mercosur deal (formally signed in January 2026) includes agricultural safeguards like tariff suspensions if imports exceed 5%. Meanwhile, EUDR deforestation rules have been delayed until December 30, 2026, with simplifications for EU operators.

Sector implications

The report points to continued growth in 2026 for EU poultry, with export growth of around 2% and production growth of 1.3%. Poland remains the leading producer, although disease and environmental constraints persist in parts of the EU.

Source

European Union: Poultry and Products Semi-annual, USDA Foreign Agricultural Service (FAS).

https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Poultry%20and%20Products%20Semi-annual_Paris_European%20Union_E42026-0019.pdf