Part 1 – Laying hen husbandry, egg production and egg trade

In two papers, the patterns of the EU poultry industry will be analysed. The first paper deals with laying hen husbandry, egg production and egg trade. The second paper will document the patterns and dynamics of poultry meat production and trade.

Hans-Wilhelm Windhorst – The author is Professor em. at the University of Vechta and visiting Professor at the University of Veterinary Medicine, Hannover, Germany

In 2020, the 27 member countries of the EU shared 7% in the global laying hen population and contributed 7% to global egg production. They played a major role in egg trade. Over 50% of the globally traded eggs originated in one of the member countries, and over 40% of the imported eggs had a member country as destination. Here, the intra-EU trade is included.

High regional concentration in layer flocks and egg production

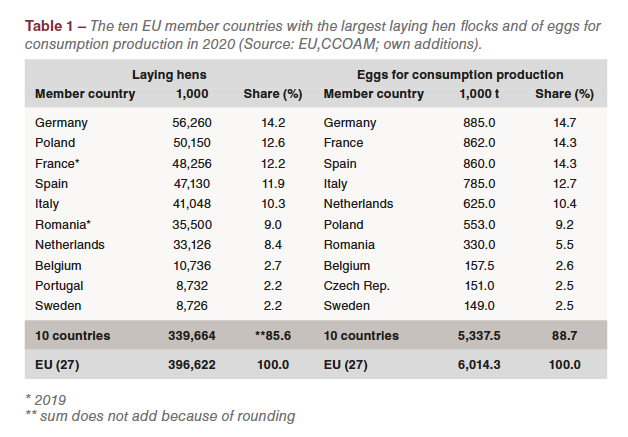

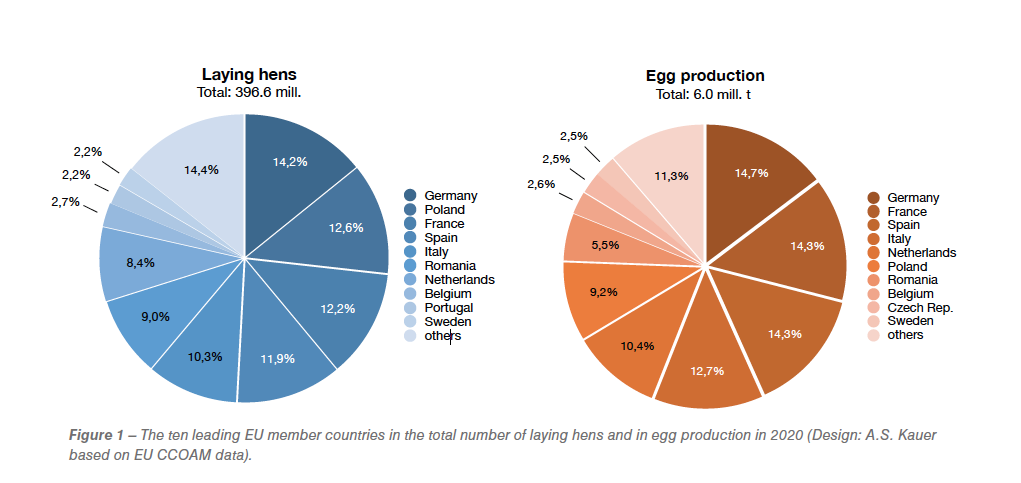

In 2020, 396.6 mill. laying hens were kept in the EU, of which about 36 mill. were hens for producing hatching eggs. The data in Table 1 and Figure 1 document the high regional concentration. The ten leading countries shared 85.6% of the total layer flock, the top five countries even 61.2%. With 56.3 mill. hens, Germany held an unchallenged first rank, followed by Poland and France.

Table 1 also shows that the regional concentration in egg production was even higher. The ten leading countries contributed 88.7% to the overall production volume of the EU, the top five countries 66.4%. A comparison of the composition and ranking reveals some remarkable insights. The shares of the countries in the number of laying hens and in egg production differed considerably. Germany’s contribution to egg production was for example only 0.5% higher than its share in the laying hen flock of the EU. In France, Spain, Italy and the Netherlands, the gap between the share in the laying hen flocks and in egg production was much wider. An imbalance can be observed for Romania. The number of laying hens, as reported by the EU Commission, cannot be correct, as it would demand an average laying rate of over 600 eggs per hen and year. According to FAO data, the number of laying hens in Romania in 2019 was 35.5 mill. The annual laying rate would be 125 eggs. This is more realistic, as about 80% of the hens were kept in small family farms and only 20% in farms with efficient management systems.

Considerable differences in the share of housing systems

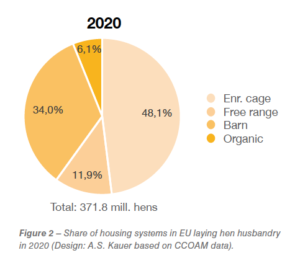

Four housing systems are permitted in the EU: enriched cages, barn resp. floor systems, free-range systems and organic systems. Two of the 27 member countries, Austria and Luxembourg, no longer allow enriched cages and they will be prohibited in Germany from 2025 on. The share of the housing systems differed considerably between the single member countries.

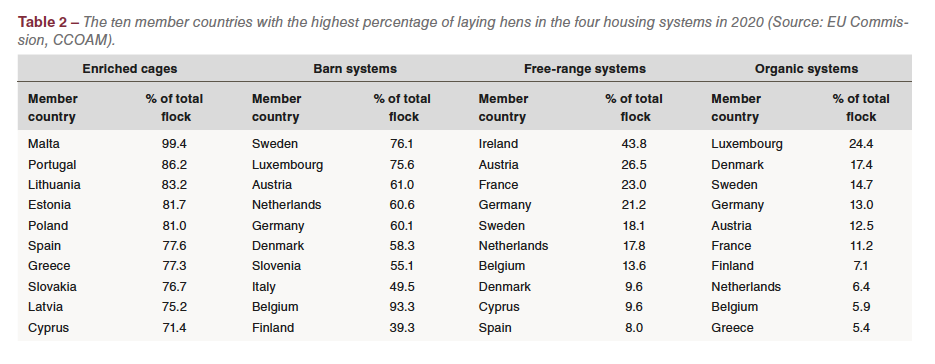

Figure 2 documents that in 2020 48.1% of the hens were housed in enriched cages, 34.0% in barn systems, 11.9% in free range and 6.1% in organic systems. Enriched cages dominated in most of the Eastern and Southern European countries, barn systems in Northern and Central Europe, free range systems reached high shares in Ireland, Austria, Germany and the Scandinavia countries. Four member countries had not installed organic systems in 2020 (Bulgaria, Latvia, Slovakia and Malta), higher shares showed Luxembourg, Denmark, Sweden, Germany and France (Table 2).

The percentages as documented in Table 2 have, however, to be valued in relation to the total number of laying hens in a specific country. The highest absolute number of laying hens in enriched cages in 2020 had Poland with 45.6 mill. birds. In barn systems, Germany ranked in first place with 33.8 mill. hens; this was also the case in free-range systems (11.9 mill. hens), followed by France (11.0 mill. hens), and in organic systems (7.3 mill. hens).

The average laying rate of hens in the various housing systems and member countries varied considerably. The difference between enriched cages and barn systems has narrowed over the past decade and hybrid hens lay about 300 eggs per year. In free-range and organic systems, the average laying rates are lower. In free-range systems, the average varies between 280 and 290 eggs per hen and year and in organic systems between 270 and 280 eggs.

Spatial patterns of egg trade with non-EU countries

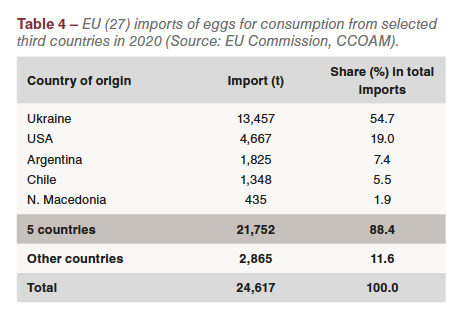

The volume of egg trade between EU member countries was much higher than with non-EU countries. For example, Germany imported 376,000 t of shell eggs for consumption in 2019, and the Netherlands exported 318,400 t. In comparison, EU member countries exported 250,324 t to so-called third countries (Table 3) in 2020 and imported only 24,617 t from third countries (Table 4).

As can be seen from the data in Tables 3 and 4, the regional concentration in imports was much higher than in exports. Because of the high self-sufficiency of the EU for eggs, it has been stable at about 105% for years, only small amounts of eggs were imported. The imported eggs were mainly further processed in the egg products industry and mostly produced in conventional cages.

The leading countries of destination for egg exports were located in Asia and Africa. The eggs were shipped in refrigerated containers and either further processed in the egg products industry or sold for direct consumption.

The percentage of traded eggs with third countries was extremely low. Only 4.1% of the produced eggs was exported to non-EU countries and less than 0.1% of the consumed eggs was imported from third countries. This documents that egg trade with non-member countries was only of minor importance for the EU (27).

Summary and perspectives

The preceding analysis could document that the regional concentration of laying hen husbandry and egg production was very high in the EU (27). Over 60% of the laying-hen flock was kept in only five member countries and the leading five countries contributed over two thirds to the total egg production volume. Regarding the housing systems, great differences existed between the 27 member countries. In total, 48.1% of the housed laying hens were kept in enriched cages, 34.0% in barn systems, 11.9% in free-range systems and 6.1% in organic systems. The trade with shell eggs for consumption with third countries was only of minor importance for EU member countries. The trade volume between member countries was much higher, especially between the Netherlands and Germany.

One can expect that the egg production volume within the EU (27) will remain stable over the coming years and no major changes in the regional pattern will occur. What impacts a banning of conventional cages in countries outside the EU (27) will have on egg trade is almost impossible to predict.

Data sources and suggestions for further reading